Yahoo Finance

Yahoo Finance What are the implications of taking your pension at 55?

As a pension saver, there are now a host of different options to choose from when you turn 55.

This is thanks to the “pension freedoms”, reforms first announced 10 years ago, which allow people to access their retirement savings more flexibly – including being able to cash in their entire pot in one go.

That said, just because you are able to draw an income – or take tax-free cash – from your pension at 55 (going up to 57 in 2028), it doesn’t necessarily mean you should.

If you don’t feel confident about knowing what to do when you reach this age, you’re not alone. Studies repeatedly show that many people feel overwhelmed at the thought of having to make a decision.

Here we help you understand the various options – and which one might be right for you:

How much pension can you take tax-free at 55?

Under rules which took effect in 2015 you can start taking your pension from the age of 55.

While this has given people flexibility and choice, it’s also given them responsibility over managing their retirement savings.

When you come to access your pension, up to 25pc can usually be taken as tax-free cash.

Charlene Young, pensions and savings expert at AJ Bell said: “You might have plans for the cash, including using it to top up your income tax-free. But many people don’t realise you don’t actually have to take it all in one go.”

What you don’t take out can be left invested in your pension where it can continue to grow tax-free, and then be used to give you chunks of tax-free cash when you need it.

How much will you lose if you take a lump sum?

If you do decide to cash in your whole pension pot, you need to be aware that taking more than 25pc in one go will mean some income tax will probably need to be paid. With greater withdrawals comes a greater chance of being landed with a large tax bill.

Not only this but if you start drawing from your pension too early, or take too much, there’s a risk you won’t have enough to live comfortably in retirement.

Helen Morrissey, head of retirement analysis at Hargreaves Lansdown, said: “Taking money out of your pension at age 55 means it has less time to grow. This could impact how much income you can take.”

If, say, you take out your full allocation of tax-free cash at this point, this will make a significant dent in your overall pension position.

Ms Morrissey added: “It may mean you need to make budget cuts later on.”

If you are wondering “how much will I lose if I take my pension at 55” then read on.

What you can do with your pension at 55

Here’s a rundown of the main options you can choose from:

Income drawdown

With income drawdown, you can access some of your money while leaving the rest invested to continue growing – with the aim of growing the pot for years into the future through investment returns.

You can take up to 25pc of your savings tax-free and can decide either to take this as a lump sum upfront and leave the remainder where it is, or you can opt to have a regular monthly income.

Alternatively, you can simply withdraw ad hoc lump sums as and when you want.

There are scenarios where this flexibility can be particularly helpful. Say, for example, you experience a change in circumstances, you can tweak the level and frequency of the payments as required.

Andrew Tully, technical services director at Nucleus Financial, said: “Drawdown will remain the key retirement solution for many as it gives the flexibility to cope with changing needs in retirement. Given the ongoing freezing of the tax thresholds, being able to vary income to ensure it is taken as tax efficiently as possible is a key benefit.”

That said, if you do opt for income drawdown at age 55, you need to be careful to manage your withdrawals over this prolonged period of time.

Ms Morrissey added: “Taking out too much on a sustained basis can severely deplete your pension and leave you struggling for cash.”

You also need to think carefully about the tax implications of the drawdown decisions you make.

Taking a large withdrawal from your pension could result in you being hit with an unnecessary tax bill that could be avoided by steadily drip-feeding withdrawals.

Buying an annuity

Annuities were once the go-to option when it came to funding retirement. These insurance contracts convert your savings into an annual pension, giving you an income for life. This income is taxable.

Since the pension freedoms came into play, offering savers more flexibility, annuities have dwindled in popularity.

That said, if you are looking for the certainty and security of a guaranteed income on top of the State pension, an annuity could still be the right option for you – especially now that rates have improved.

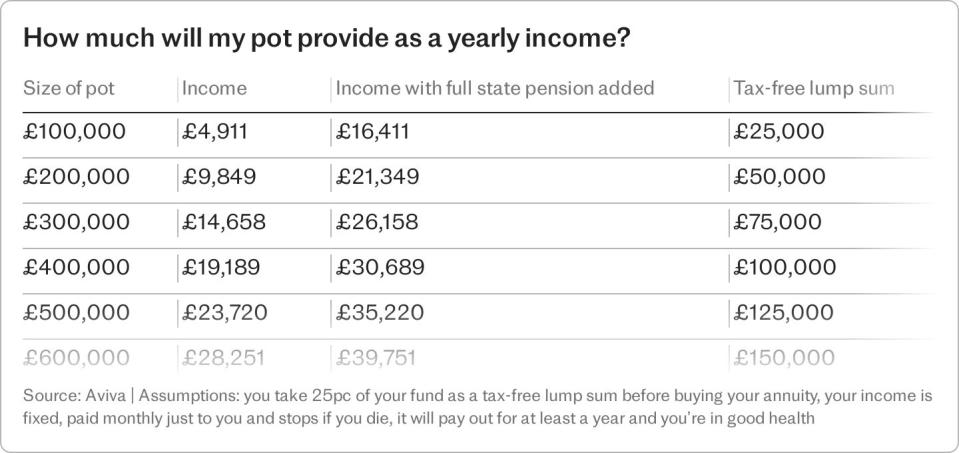

If, for example, you want the peace of mind of knowing essential costs will get paid you might want to opt for an annuity. At today’s rates £100,000 will buy a 65-year-old around £7,500 a year of income for life.

It’s also worth noting that if you smoke or have a health condition you could be entitled to higher rates – via an enhanced annuity. These tend to pay more because providers expect to pay out over a shorter period of time.

Pete Cowell from Standard Life, said: “What many people don’t realise is that enhanced annuities can often provide a more generous income to those suffering from health conditions or shorter life expectancy. The value and security they offer makes them hard to overlook, especially for those with health conditions.”

The downside of annuities is that the rate is generally fixed and the income dies on the death of the holder or their partner.

Money left in a drawdown account on the other hand can cascade down the generations free of inheritance tax and potentially free of income tax too.

The hybrid option

In addition to the options set about above, you could take a mixed approach.

This could, for example, involve you taking out an annuity to cover essentials such as your mortgage or household bills, while drawing the rest of your income from a drawdown account.

Ms Morrissey said: “This can be a good way of covering your needs while giving the rest of your pension room to grow.”

Other experts agree this is an option well worth considering.

Mr Tully said: “Blending drawdown with a guaranteed income may give a better outcome than solely using an annuity.”

Equally, if you want more flexibility now (and are in good health), along with more security later, you might find the best option is to delay buying an annuity until later in life.

This would allow you to benefit from the higher rates generally offered to older people.

Can you take your pension and still work?

There is nothing to stop you taking your pension once you reach age 55, but then continuing to work. These days there is no set retirement age; you decide when you want to stop working.

You could even choose to use your pension to support you while you are still in a job. This might, for example, enable you to reduce your working hours and go part-time.

The key thing to remember is that if you do opt to take some of your pension savings while you are working, you need to ensure you will have enough to live on when you do eventually decide to stop.

Be warned – once you take more than the tax-free amount, your ability to save into a pension going forward is severely curtailed. The usual £60,000-a-year annual allowance drops to just £10,000.

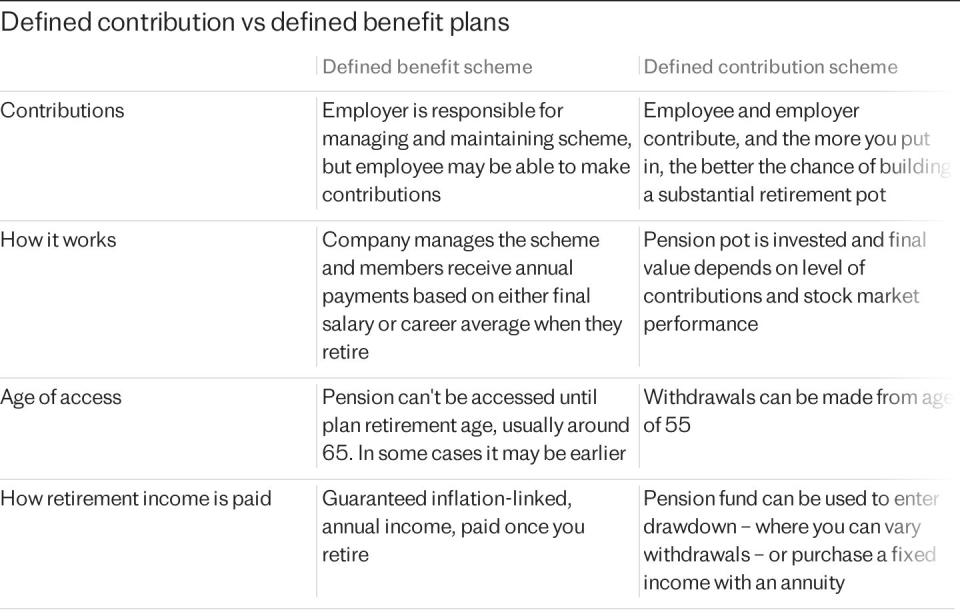

Defined contribution vs defined benefit pension

As a saver you need to be aware the options laid out above apply to “defined contribution” (DC) pensions. With a DC pension, the final payout is determined by the money invested during your working life, and how well the investments have performed.

If you have a “defined benefit” (DB) pension, the rules will be different. With a DB scheme, also known as a “final salary” or “career average” pension, you are promised a certain guaranteed inflation-linked income each year when you retire. This is the case, irrespective of the performance of the investments.

Ms Morrissey said: “If you have a DB pension, check with the scheme whether you can take your income from age 55.”

Also be aware that as a DB scheme will pay out a guaranteed income for life – which rises annually – you will not have the option of using income drawdown.

Do you need financial advice?

Given that the decisions you make in regard to your pension pot at 55 will have such a huge impact on your standard of life once you stop working, for some people it might be worth speaking to a financial adviser.

After all, you’ve worked long and hard to amass that fund – and will want to ensure it lasts as long as possible.

Recent figures from the Financial Conduct Authority show that 58pc of pensions accessed in 2022-23 did not receive advice or guidance. In many of these cases that will be fine – cashing in a small pension pot to clear a mortgage or loan may not require paying an adviser to help you.

Stephen Lowe from retirement specialist, Just Group, said: “Retirement decisions are some of the trickiest financial decisions that people will ever face.”

With a range of options available, you may feel poorly equipped and feel more comfortable paying an adviser for help with pension rules, tax implications and investments if you are going to use a drawdown account.

Note that you can also get help from PensionWise, a service from government-backed Moneyhelper, which offers a free appointment to those aged over 50 who have a DC pension pot.

These appointments will help explain your options, but they will not be able to give tailored, regulated recommendations.