Yahoo Finance

Yahoo Finance How to top up your state pension

As a guaranteed income that rises every year, the state pension is a staple part of most retirees’ budgets. Around 12.6 million people now receive it and many depend on the money to see them through their golden years.

The Pensions and Lifetime Savings Association puts the cost of a “minimum” no-frills retirement at £14,400 for a single person and £22,400 for a couple. If you’re single, this year’s full new state pension will get you 80pc of the way there, and if you’re a couple and both claim, you’ll pass the threshold comfortably.

Only around half of people receive the full new state pension, and for the old state pension, the proportion is only 74pc. Luckily, it’s just become easier to “top up” what you receive.

Here, Telegraph Money runs you through how to boost your state pension payments, and how much it will cost you. This guide will cover:

Can you increase your state pension?

The amount of state pension you receive depends on a few factors, including when you reach or reached state pension age and, chiefly, how many full years of National Insurance contributions (NICs) you’ve made by the time you reach it.

The new state pension is for men born on or after April 6 1951 and women born on or after April 6 1953. To qualify for anything, you’ll need at least 10 years of NICs and to get the full amount, it’s 35.

Although most people work for at least 35 years, many don’t. There are various reasons why you might not get 35 qualifying years. For example, you might have been a low earner who did not pay NICs, out of work and not claiming benefits, self-employed with low profits, working part-time or living abroad.

Any of these situations can create gaps in your National Insurance record – and could mean you get a lower state pension as a result.

If you’re in this situation, you do have options to fill these gaps, and one of those is buying voluntary NICs. However, this comes with a range of considerations

If you’re on the “old” basic state pension, which will be the case if you reached state pension age before April 6 2016, it is too late to top it up through voluntary NICs.

What are voluntary National Insurance contributions?

Voluntary NICs are a payment from you to the Government to top up missing years of NICs. By adding enough to complete a year, you could add up to £328.64 to your annual state pension income. This lasts as long as you live.

To benefit from this, you need to top up your contributions to a full year – partial years don’t get you anything. However, if you have already made partial payments during a given year, it wouldn’t cost you a full year’s contributions to top that up. The actual amount could be anything from one week’s contribution to the full 52.

You can also keep adding more completed years up to the maximum of 35, which would take you to the full state pension.

However, there are limits, and topping up won’t always increase your income. For instance, if you reach 35 years of contributions anyway, topping up any previous incomplete years won’t make any difference. There are also pension credits to consider – more on that later.

How to top up your state pension through voluntary contributions

The first step is to check your National Insurance record. The easiest way to do this is online, but you can ask for a statement by phone or by post. This will allow you to identify any gaps. You should also check your state pension forecast to see how much you’re currently on track to get, and when you’ll get it.

The Future Pension Centre can also help you work out whether making voluntary payments will increase your state pension – because sometimes it doesn’t. For example, if you contracted out of a Serps additional state pension scheme, there will be a point where no extra contributions can be made, as you’ll already have reached the “flat rate” of pay available.

Before making any payments, you should also check if you’re eligible for National Insurance credits. You may be able to top up years without making a payment, particularly if you weren’t working due to being a carer or looked after children.

If you’ve worked out that you do have gaps and decide it’s worth making a voluntary contribution, you’ll need to make the payment. If you’re a worker, you can now do this online or via the HMRC app using the “Check your State Pension forecast” service – note that you’ll need to login using a government gateway account. You can also use this service from abroad, but only for years you were resident in the UK.

If you’re self-employed, already receive the state pension or live abroad and want to make payments for those other years, you’ll still need to call HMRC.

Who is eligible?

Whether you can top up, and how far you can go back to fill any gaps, depends on your circumstances.

Usually, you can top up any gaps in the previous six tax years. However, until April 5 2025, the Government is allowing top-ups right the way back to April 2006. As soon as this deadline passes, you’ll only be able to top up the previous six tax years again.

You can’t usually top up if you don’t have any gaps during these years. There are also restrictions if you’re a married woman or widow paying reduced rate National Insurance.

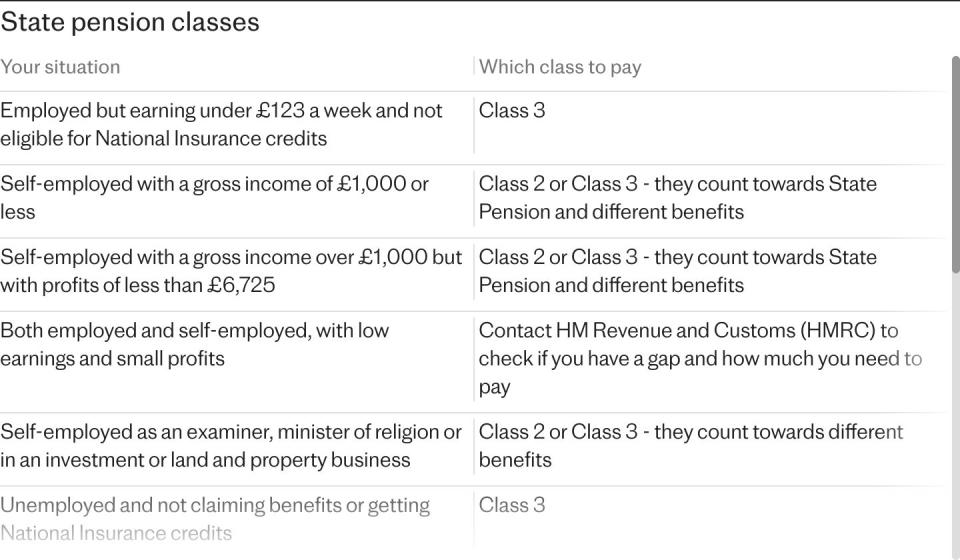

The way you need to top up, and how much, also varies depending which class of NICs you pay.

You can still top up your state pension even if you’ve reached state pension age and started claiming it. However, you’re subject to the same limits of which years you can top up and the payment only starts from when you make a payment – you can’t backdate it.

If you live abroad, or you used to, you may be able to pay voluntary Class 2 or 3 contributions if you either previously lived in the UK for three years in a row or paid at least three years of NICs. You should contact HMRC if this applies to you.

How much does it cost?

For the 2024-25 tax year, the cost per week is £3.45 for Class 2 contributions, and £17.45 for Class 3. If the gap in your record was between April 6 2016 and April 5 2023, you’ll pay the rates that applied in the 2022-23 tax year – for Class 2 this is £3.15 per week, and it’s £15.85 for Class 3.

These top-ups could pay for themselves – assuming you live long enough.

Sarah Pennells, of Royal London, said: “Assuming a man would live for 17.3 years after he received his state pension at 66, based on the ONS longevity data and assuming no rise in the state pension in that time, he would receive over £5,600 extra in payments, whereas a woman would receive over £6,500 extra, assuming she lived for 19.8 years after state pension age.”

This is likely to be even higher, given the state pension is protected by the triple lock guarantee, which means it rises by the highest of inflation, wages or 2.5pc.

When should you consider topping up your state pension?

Deciding whether to pay for voluntary NICs is an important decision, particularly because there’s no automatic right to a refund if you change your mind. It can also be a gamble because you might pay out more than you actually get back in extra state pension payments.

One situation where it’s usually worth it is when you’re nearing state pension age and you know you’re not going to get enough qualifying years.

Rob Morgan, of wealth managers Charles Stanley, said: “If you only have a few years to go, and you are not going to reach a full entitlement, then it makes sense to consider paying to fill in the blanks. Those that have already reached state pension age and have found they have missing years can also benefit.

“A modest outlay could boost a state pension income by hundreds, and in some cases thousands of pounds, a year. It potentially represents a far better rate of return than any other way of using savings.”

In some cases, it could even be a very small amount to top up a particular year – as little as a single week.

Mr Morgan continued: “Look out for years where you have worked part-time or for only part of the year. In these circumstances you may have paid NI, but not quite enough to obtain a year’s credit.

“Building your record for the state pension is binary, you either accrue a year or you don’t, and where you have been close to attaining one for a particular year it may be possible to pay a very small amount of money to top that year up.

“There are several pitfalls though, not least because the state pension rules have changed over the years and led to a system that can be fiendishly complicated. Don’t rely on information you have heard down the pub. Everyone’s NI record is different and what applies to someone else might not necessarily apply to you.”

If you are successful in boosting your state pension payments, you’ll need to think about how the increased income affects your financial position.

First of all, if you already pay tax on your income, you’ll pay it on any state pension increase, too. The extra money may even push you into the next tax bracket, or mean you pay tax when you didn’t before, which could affect your calculations.

If topping up your NICs does increase your income, this could also affect your eligibility for pension credit if you claim it, along with other benefits you receive. You should factor this into your decision carefully, as it may end up costing you money overall.

Another factor is your life expectancy. If you top up an entire year, you’d need to live for almost three after reaching state pension age to make back your money.

Mr Morgan said: “Whether it is worth paying for top ups does hinge on life expectancy, but you don’t have to live very long beyond state pension age for it to be highly beneficial. It is almost always worth considering if you’re close to state pension age and you know you won’t be able to get the qualifying years you need to get the full amount.”

However, Ms Pennells added: “If you have a health condition that’s severely life-limiting, you may not live long enough to see a return on your investment.”